- Africa and the EU find themselves at the heart of intensifying global competition over energy flows, as the war in Iran disrupts global markets. Meanwhile, the US pursues fossil fuel dominance and China leads in renewable supply chains, requiring both continents to navigate external pressures while shaping their respective energy futures.

- The EU has an opportunity to secure mutual benefits by partnering with Africa on small-scale hydropower, wind and grid development – creating markets for European technologies that align with Africa’s energy and industrial needs.

- Stronger cooperation could boost Europe’s supply chain resilience, complement critical minerals agreements and deepen labour collaboration through skills transfer. Yet despite its potential, sub-Saharan Africa remains the least electrified region in the world. Cheap Chinese solar is driving uptake, but weak grids, financing gaps and fossil fuel reliance still constrain progress.

- This Brief is part of the Africa Next series, dedicated to examining forward-looking themes and policies crucial for the Africa-EU partnership.

The EU has an opportunity to build a win-win energy partnership with Africa. It is well placed to be part of Africa’s power choice at a critical moment in global energy contestation. As the United States seeks to dominate trade in fossil fuels and China leads in renewable energy production, both the EU and Africa need to navigate increased competition over energy supplies and value chains. The war in the Middle East has only made matters more urgent by testing energy and value chain resilience. Such a partnership may not only boost Africa’s growth and industrialisation prospects, but also create opportunities for Europe’s energy industry. Through the Global Gateway, Team Europe should scale up hydro and wind projects, leveraging European expertise to build local skills and value creation in Africa.

Africa is at a pivotal moment in shaping an energy future central to its development and industrialisation ambitions and increasingly aligned with climate goals. Renewable technologies, including solar photovoltaic (PV), could unlock the continent’s vast energy potential. While there are signs of a solar boom in the making as imports of panels surge, solar PV alone will not turbocharge Africa’s development aspirations. Instead, the continent’s energy landscape will require a mix of renewables, such as wind and hydropower, alongside better energy system integration.

As the EU grapples with its own domestic energy choices, its global climate and energy vision, released in October 2025, positions it as a reliable partner for sustainable and resilient growth. How the Africa-EU partnership leverages this convergence, and how the EU responds to Africa’s power choices, will have profound implications for both continents in the years ahead. Investment in renewables, grids and balanced supply chains can deliver shared gains and reinforce mutual self-reliance in critical infrastructures.

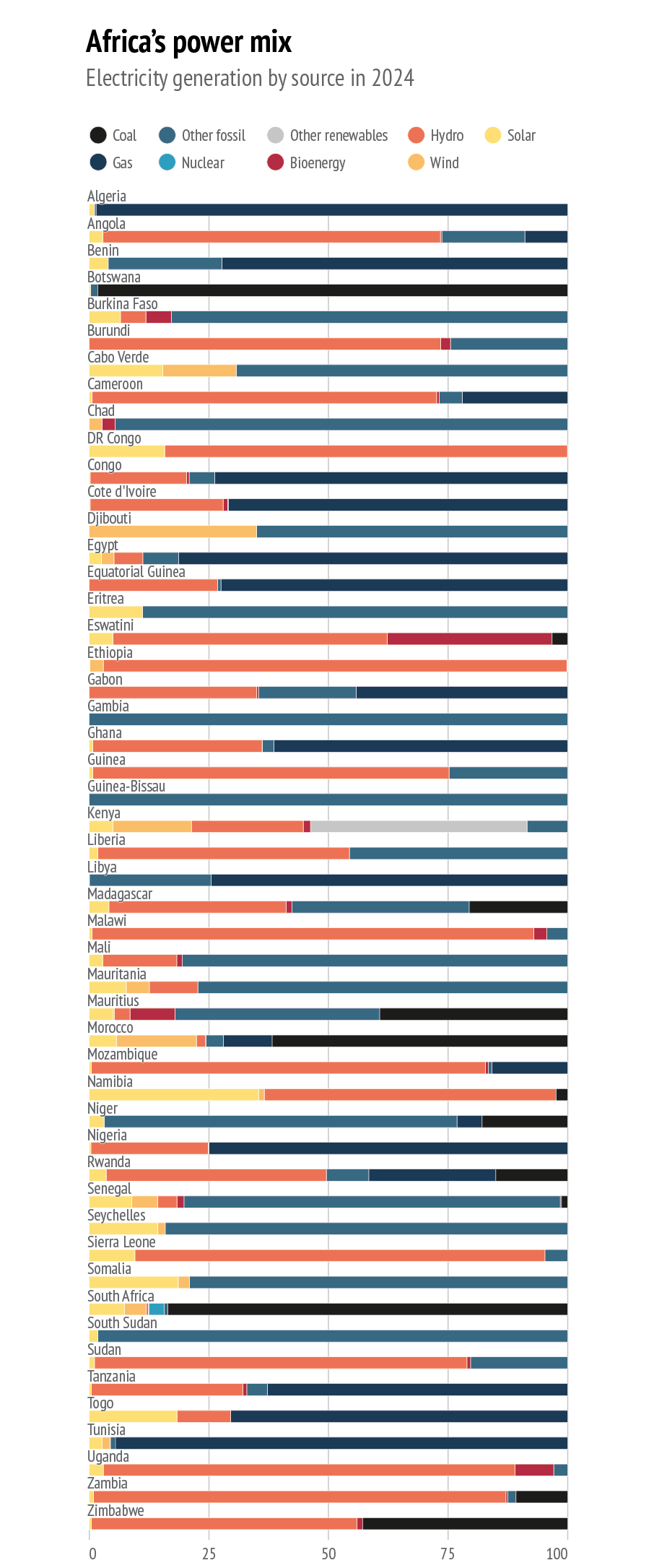

Africa's energy mix

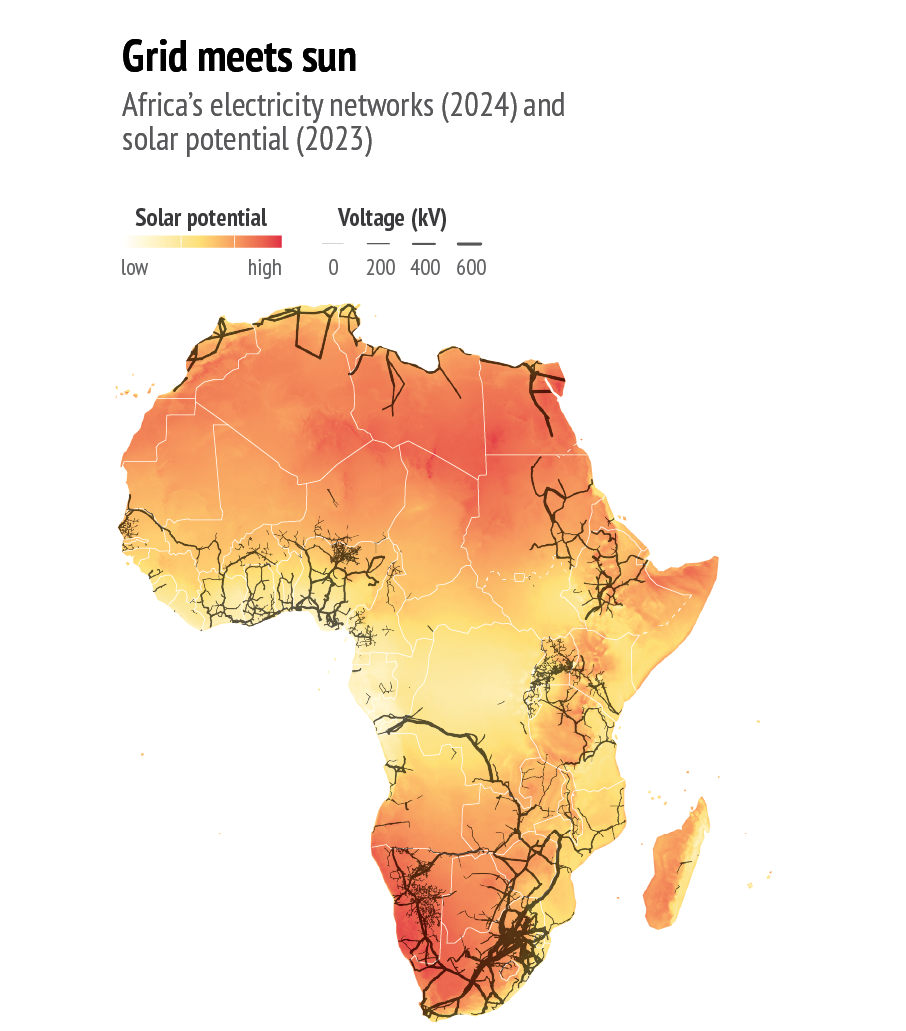

The African continent has huge, untapped energy resources. It is estimated to account for 39% of total global renewable energy potential and 60% of the world’s best solar capacity(1). However, over the past decade, more than half of investment has gone into fossil fuel extraction, primarily intended for export(2). Investment in renewable energies, including from venture capital, remains limited due to modest returns and constrained by weak and inconsistent demand.

Nevertheless, African countries and continental financial institutions are placing increasing emphasis on renewable energy. Agenda 2063, and the establishment of the African Single Electricity Market and the African Continental Master Plan, set ambitious goals for expanding energy access through regional integration while underlining the importance of renewables. The African Development Bank (AfDB) and the African Union Development Agency (AUDA-NEPAD) have key roles to play through the financing of infrastructure programmes – often co-funded by the EU and other partners – and promoting market integration and regulation(3). Facing both the severe impact of climate change and the need to advance industrialisation, expanding domestic markets and increasing purchasing power, African countries and regional institutions are increasingly viewing their natural wealth not only in terms of minerals but also energy provision.

A solar revolution?

Mass solar PV production, over 90% of it concentrated in China(4), is reshaping Africa’s energy landscape, but constraints remain.

Two main factors are driving the solar boom. One is supply, as cut-throat domestic competition in China and generous state support have reduced the cost of solar panels by 90% since 2000(5). This has upended the global market, making solar generation widely available and cheap. The other is demand. In the past three years, Pakistan, for example, has increased the share of solar in its electricity generation from zero to 20%, driven largely by households installing cheap panels in response to unreliable and costly grid supply.

In Africa, historically, major energy investments have focused on large-scale fossil fuel or hydropower projects led by governments rather than citizens. Weak electricity grids have also limited access to electricity in many homes. Thus, diesel generators powered by fossil fuels have mostly filled the gap, accounting for around 25% of total generation capacity in sub-Saharan Africa in 2019, and close to 40% in West Africa(6).

However, in 2025, Africa imported 60% more solar panels than the year before. In the last two years, data shows that solar PV imports outside of South Africa have almost tripled. In 2025, Sierra Leone imported enough solar panels to account for 68% of the country’s total generation capacity, if fully installed(7). The biggest importers are South Africa and Nigeria which together account for almost half of total capacity (5.5 GW). In both countries, centralised national utilities have struggled to meet demand, while high electricity needs and widespread use of diesel generators – especially among higher-income consumers – have driven uptake.

In Nigeria, an estimated 22 million small backup generators were in use in 2024, with a combined capacity of 42 GW – enough to power around 42 million homes(8). Almost a quarter of generators are in Lagos, despite the city accounting for only about 10% of the country’s population. In South Africa the generator market was valued at $130 million in 2025, with 35% concentrated in Gauteng and 19% in the Western Cape, the country’s wealthier regions(9). Solar PV deployment is also highly uneven, with 67.4% concentrated in the Northern Cape compared with 8.1% in Gauteng(10).

Mali has also seen a surge in solar and battery imports, especially in Bamako, triggered by the ongoing fuel blockade imposed by the al-Qaeda-affiliated group Jama’a Nusrat ul-Islam wa al-Muslimin (JNIM). Since September 2025, this blockade has created severe fuel shortages, pushed black-market diesel prices to a peak of 7.5 euros a litre in November 2025, and led to rationing at petrol stations(11). In parallel with this ‘solar boom’, Chinese exports of electrical batteries to Mali have also soared, becoming the largest single export by value in October 2025(12). Mali thus illustrates a self-contained shift towards solar adoption, primarily driven by necessity in the absence of viable alternatives.

Boom and bottlenecks

Solar does not produce dispatchable power. Without storage, it plays a limited and potentially destabilising role in underdeveloped grids.

Nigeria and South Africa have recently updated energy policies aimed at increasing energy access and moving towards green technologies, thus reducing their dependency on oil and coal respectively. While gas remains part of the mix as a ‘transitional fuel’, both countries’ longer-term ambitions centre on renewables(13).

In South Africa, due to long-standing grid constraints citizens and industry have had to contend with rolling blackouts. In this context, local solar panels have helped minimise reliance on diesel generators in households. However, solar panels are also adding complexity to the grid, further straining the electricity system.

In Nigeria, efforts to diversify away from an unreliable fossil fuel-powered grid have encountered similar problems with integrating solar PV(14). While there has been progress in using solar power in public infrastructure and developing local microgrids, scaling these solutions remains a challenge.

The EU and Africa's power future

The EU can play two key roles in unlocking Africa’s energy future, including through the Global Gateway. It should promote its strategic, economic and business interests, while supporting African industrialisation. European policy should focus not only on development, but also on fostering market creation through joint ventures, capacity building and job creation.

The first is to complement the solar boom in areas where the EU is strong and competitive, namely wind and hydropower. The EU, via the Team Europe initiative, has already been active on hydropower through the Global Gateway, including the Nachtigal dam in Cameroon and the Ruzizi III plant spanning the DRC, Rwanda and Burundi. However, more attention to smaller projects, such as run-of-river, would dramatically upscale regional capacity at lower cost. In wind energy, the EU is competitive but faces competition from cheaper Chinese providers. Its edge lies in large-scale and offshore projects.

For both wind and hydropower, a clearer ‘Made-in-Europe’ strategy should be put in place to compete for tenders. There is also scope for a more explicit transactional approach: for example in wind energy, where critical minerals needed for permanent magnets are often mined in Africa but refined in China, undermining European competitiveness. EU-funded energy projects could therefore be combined with critical mineral partnerships, creating a more equitable and stable supply chain for Europeans while also developing value addition in Africa.

The second is system integration to better harness electricity for industrial development. Across sub-Saharan Africa, limitations in the grid infrastructure constrain both development and large-scale electrification, a problem that Europe has also faced. Europeans are already ahead in integrating higher shares of renewable energy into power grids, with several system operators deploying technologies capable of operating grids on 100% renewables. European companies also bring expertise in power flexibility and demand-side management based on consumer behaviour rather than centralised state control, making them more aligned with Africa’s bottom-up power choices.

There are additional areas of mutual benefit. Firstly, the EU has many grid equipment manufacturers which are already scaling up production for the domestic grid. Demand from African countries would enable even greater economies of scale and strengthen competitiveness vis-à-vis China. Secondly, as European grid operators and utilities grapple with manpower shortages, training a workforce to operate grids similar to those in Europe could allow European system operators to tap into skilled labour in the future while contributing to develop the sector in Africa. Such partnerships offer clear mutual gains, especially as Europe seeks to enhance the resilience and security of its own grid.

Ultimately, an empowered Africa offers the EU greater investment opportunities, a rapidly growing market, and the prospect of bringing value chains closer to home. Converging agendas on renewables and just energy transitions can only benefit both continents. In both grid equipment and grid management technologies, the EU stands to gain, retaining a competitive edge over both the US and China.

References

* The authors wish to thank Luca Guglielminotti, EUISS trainee, for his research assistance.

1. European Commission, ‘Joint Communication: EU global climate and energy vision’, 16 October 2025.

2. IEA, ‘World Energy Investments 2025’, 5 June 2025.

3. See: AfDB Group, Map Africa; AUDA-NEPAD, ‘The African Continental Master Plan’.

4. IEA, ‘Solar PV global supply chains: executive summary’, 7 July 2022.

5. García-Herrero, A. and Mu, H., ‘China can decarbonise the world even if it won’t fix its overcapacity problem’, Bruegel, 24 September 2025.

6. Ghandi, D., ‘Deployment and use of back-up generators in sub-Saharan Africa’, Brookings, 2 October 2019.

7. Jones, D., et al., ‘The first evidence of a take-off in solar in Africa’, EMBER, 26 August 2025.

8. Stantec et al., Nigerian Market Report, May 2024.

9. Data Insights Market, ‘South Africa Diesel Generator Market Size, Share and Growth Report: In-depth analysis and forecast to 2034’.

10. Mordor Intelligence, South Africa Solar Energy Market Growth Report 2031.

11. Höije, K., ‘Bamako is grinding towards a halt’, The Continent, Issue 220, 15 November 2025.

12. The Observatory of Economic Complexity, ‘Mali (MLI) and China (CHN) trade profile’

13. Nigerian Ministry of Power, National Integrated Electricity Policy, 22 May 2025; Republic of South Africa, Energy Action Plan – One-year progress report: August 2023.

14. Alpojedje, F.O. and Ibhagbemien, A., ‘Renewable Energy Integration: The impact of solar systems in Nigeria’s power supply and reliability’, NIPES Proceedings in Science and Technology, 2025.