For years, the EU has played a prominent role in leading the world’s transition to clean energy through its robust backing for green technologies and a determined policy push to reach net zero. Initiatives such as the European Green Deal, ‘Fit for 55’ and the Net Zero Industry Act (NZIA) not only advance ambitious emissions reduction targets, but also promote clean tech that is made in Europe.

All the while, China has established itself as a clean energy juggernaut, increasingly dominating the supply chains of clean tech on which the EU relies (1). China’s meteoric rise in the clean tech sector has also coincided with an increasingly bellicose approach to diplomacy, exemplified by recurrent threats to ban critical mineral exports and the imposition of controls on exports of certain materials (2). Going forward, the EU will have to walk a fine line between meeting its climate and energy goals, while also managing its dependencies on Chinese supply chains.

Making the energy transition work

To ascertain if the EU can go green without China, a clear-eyed assessment of its industrial landscape is crucial. This can be done by examining the technologies that are key for the energy transition: solar photovoltaics (PVs), wind turbines, batteries, electrolysers and heat pumps.

Solar PVs and wind turbines are expected to cover the lion’s share of the EU’s new renewable electricity production capacity over the coming decades. Batteries should enable the electrification of the EU’s vehicle fleet and play an important role in energy storage. Meanwhile, electrolysers are key for the production of green hydrogen, which can clean up hard-to-abate sectors like steel and cement, whereas heat pumps will play a pivotal role in decarbonising buildings and light industries.

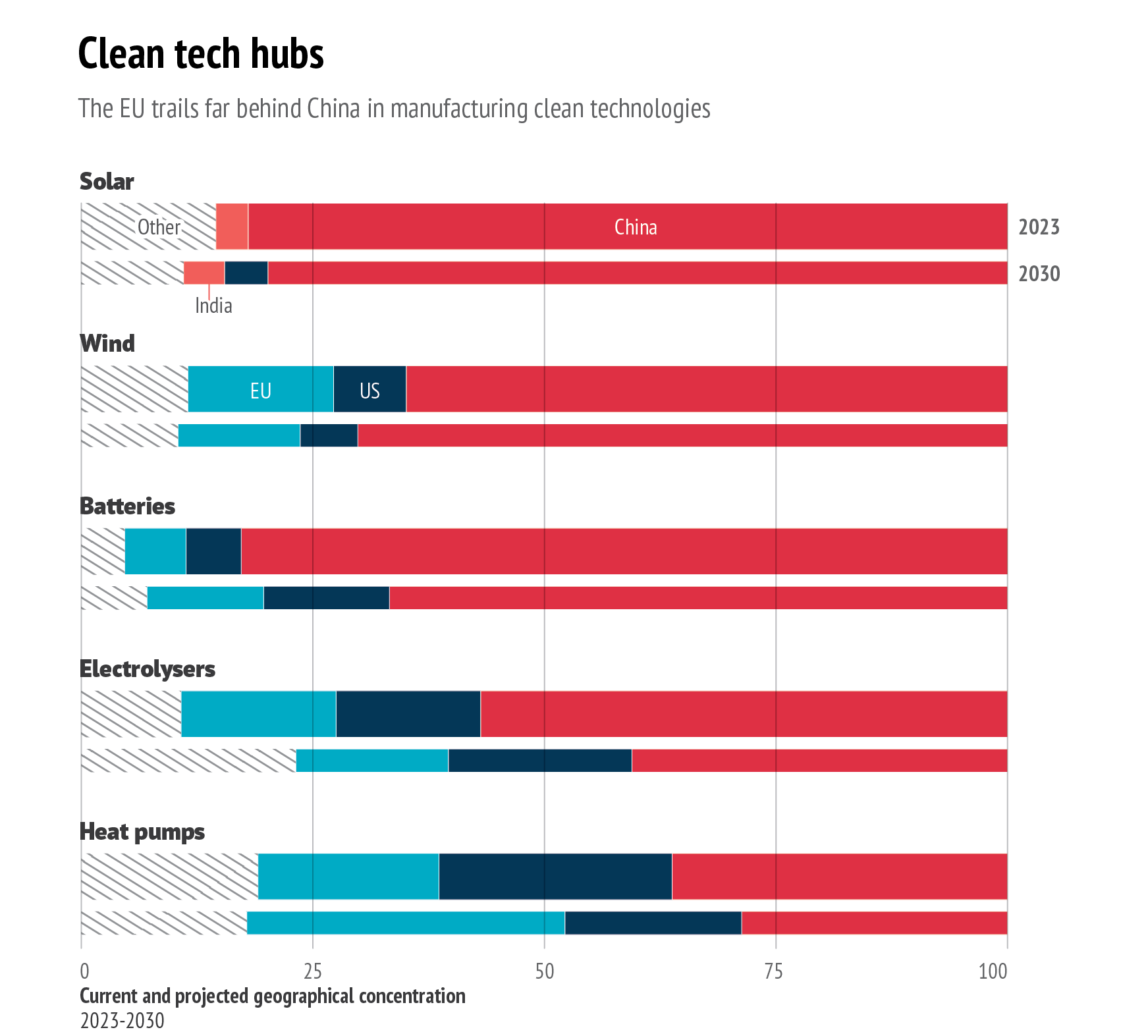

When it comes to manufacturing capacity, the EU’s industries are a mixed bag. The continent’s ailing solar PV industry sources most of its components from China (3). In contrast, wind turbine and electrolyser manufacturers have the capacity to produce well beyond internal needs (4). Europe also has a reasonably strong heat pump industry, having met 60 % of its own demand in 2022 (5).

For batteries, the verdict is not as clear-cut. At first glance, domestic battery producers were able to meet around 50 % of the EU’s needs in 2022 (6). However, most of these batteries were produced by Korean and Chinese companies that have set up their manufacturing bases in the EU.

Data: IEA, 2023

Going forward, the International Energy Agency (IEA) predicts an uptick in the EU’s global share of battery and heat pump manufacturing by 2030, alongside a slight dip in the EU’s wind turbine output, while production of other technologies is expected to remain largely unchanged. Initiatives like the NZIA, which aim to scale up the production of clean energy technologies, might change these projections in the EU’s favour, but it is still too early to say to what extent this will be the case.

A closer look at the entire value chain reveals the EU’s acute reliance on China. Beijing accounts for around 70 % of the global supply of graphite and rare earth elements and holds a near-monopoly on the processing stage of critical minerals (7). By contrast the EU is almost entirely reliant on imports to meet its critical material needs. Graphite, lithium, nickel and cobalt play an important role in the production of batteries, while rare earths are needed for permanent magnets, which are vital for wind turbines and electric vehicle (EV) motors, among other technologies.

Could this change?

In theory, the EU has many of the ingredients needed to go green without China. It has the know-how, the industrial foundations, and the policy support to pursue ambitious reshoring initiatives. Yet, for the time being, an energy transition without China would be impossible. For a start, it would take a colossal amount of investments to prop up the EU’s clean tech industry to the point where it could substitute Chinese components. According to Bloomberg NEF, Europe would need to invest an eye-watering €136.3 billion in manufacturing plants to meet 100 % of its clean energy demand locally by 2030 (8).

Moreover, it is not just the cost of building factories that would make this effort difficult. Replicating the vast, vertically integrated manufacturing ecosystems present within China would take determination and time. Also, even if the EU were to succeed in replicating China’s manufacturing capability, it would likely struggle to keep this industry competitive. The manufacturing costs of solar PVs, battery packs and wind turbines in China are 50 % (9), 40 % (10), and 20% (11) lower than in Europe, respectively. This is attributed not only to government incentives, but also reduced costs of materials, electricity and labour.

The continent’s ailing solar PV industry sources most of its components from China.

Reducing the EU’s dependence on critical materials sourced from third countries — as envisioned by the EU’s Critical Raw Materials Act — will also be no easy task. While the EU might find some of these minerals at home, strong local opposition to new mining projects casts doubt on their feasibility. Also, even if approved, any new mine would not become operational for about a decade. Moreover, this does not even account for the EU’s lack of mineral processing capacity, or the higher operating costs associated with domestic mining due to stricter environmental regulations compared to China. Ultimately, recycling minerals from used equipment will not be a scalable solution until large quantities of batteries or wind turbines reach their end of life, which estimates suggest will not happen until the second half of the next decade (12).

All doom and gloom?

At this point, there is no doubt that the EU will be unable to go green without Chinese equipment or at least access to its supply chains. While this raises valid concerns about associated geopolitical risks, it does not pose an existential threat.

For starters, being dependent on solar panel imports is not the same as being dependent on natural gas. This is because even if new solar PV shipments from China ceased today, the EU could still generate electricity from existing panels. In fact, most modern solar panels have an average lifespan of around

30 years, while solar inverters (another market dominated by China) last for up to 15 years. If China limited access to equipment containing rare earths, like permanent magnets, the deployment of new wind turbines would drastically slow down, posing a very serious challenge to their developers (13). Yet, as disruptive as this would be, it would not cause people to freeze to death or push the EU to the brink of economic collapse as the bloc could rely on existing power generation sources.

Furthermore, any Chinese effort to weaponise clean tech exports would quickly backfire. This is because it would turbocharge the EU’s efforts not only to de-risk, but to decouple from China, providing a boon for clean tech manufacturers in Europe and beyond, all while threatening the revenues of China’s export-reliant industries. For example, Europe alone spent €18.5 billion on Chinese solar products in 2022 (14). Efforts to choke off access to rare earths would also fuel the rise of alternative suppliers. The historical precedent is clear: in 2010, when Beijing threatened to halt rare earth exports to Japan due to a territorial dispute over the Senkaku/Diaoyu Islands, Tokyo responded by implementing a decisive diversification strategy. It invested in an Australian rare earths mining company with a processing plant in Malaysia, helping reduce Japan’s rare earth reliance on China from 90 % to 60 % (15).

Any Chinese effort to weaponise clean tech exports would quickly backfire.

Meanwhile, there are valid cybersecurity concerns about using Chinese-built components in critical infrastructure like power grids (16). However, the risks of using similar equipment (e.g. solar inverters) in less critical areas, while non-negligible, are less clear.

Rolling up the sleeves

The green transition will not be easy. Not only because the continent will need to overhaul its energy system, but also because it will have to live with a troubling reliance on Beijing. Even if this dependence may not be as dangerous as it initially might seem, the EU must pursue a de-risking strategy. Failure to do so would undermine the EU’s goal of becoming the home of industrial innovation and the champion of clean tech.

At least four strategies are available for Brussels to tackle its dependence on China.

First, level the playing field for clean tech companies. Concerns have existed for years regarding potential market distortions caused by Chinese government incentives. They are suspected of creating an unfair advantage for Chinese clean tech producers, potentially flooding the market with lower-priced goods. The EU needs to double down on its existing efforts to investigate if illegal Chinese subsidies have been used to distort the competition for technologies like wind turbines and EVs.

Second, prioritise innovation. Pouring funding into established technologies like solar PVs in an already over-supplied market and playing catch-up with China is one way of mitigating this risk, but maybe there is a better way forward. After all, there is the unintended likelihood that taxpayers’ money could end up going to ‘zombie companies’ that could not survive without subsidies and compete on the global market.

An alternative approach would be to invest in emerging technologies that could reduce reliance on imports and Chinese supply chains. Sodium-ion batteries represent a potential example of such technologies. They replace lithium with sodium – salt – and do not require critical materials such as cobalt, graphite and nickel for their anodes and cathodes. While these batteries come with their drawbacks, such as lower performance, they nonetheless could play an important role in the EU’s bid for greater strategic autonomy.

Third, focus on international cooperation. Despite efforts to boost domestic production and encourage material substitution, the EU will likely remain heavily reliant on critical material imports for the foreseeable future. Signing strategic partnerships with international partners is a promising start, but many of these agreements lack binding commitments. Therefore, the EU should pursue long-term measures such as fully-fledged trade or investment agreements with resource-rich countries, while also discouraging trade partners from adopting dual pricing mechanisms, export restrictions, quotas and other tools that could prevent market access and equal treatment.

Furthermore, the EU should harness the full potential of initiatives like the Critical Raw Materials Club, which aim to strengthen global supply chains among like-minded partners. Although it is still unclear to what extent such initiatives can encourage deal-making, they can nonetheless promote knowledge exchange, best practices sharing and support capacity building.

Fourth, consider stockpiling critical materials. A critical materials stockpile would serve to cushion the impact of short-term supply disruptions. This stockpiling could be done either through direct government action or public-private partnerships. In fact, the EU would not need to reinvent the wheel. Japan has a long-standing cooperative stockpiling system operated between the government and private sector, ensuring natural resource and economic security. Managed by the Japan Oil, Gas and Metals National Corp (JOGMEC), the government prioritises and decides on the exact stockpiling quantities out of a list of 34 minerals (17).

In the end, even though going green without China may be impossible at the moment, this does not have to be a reason for despair. If one thing is abundantly clear, it is that the EU has a wide array of strategic options at its disposal to advance its green agenda.

References

1. Simon F., ‘As global clean energy champion, China has “responsibility” to lead at COP28: IEA’, Euractiv, 30 November 2023 (euractiv.com/ section/energy-environment/news/as-global-clean-energy-champion- china-has-responsibility-to-lead-at-cop28-iea/).

2. ‘China threatens to curb mineral supply to West amid widening tech war’, Politico, 4 July 2023 (politico.eu/article/china-beijing-threaten- curb-mineral-supply-to-west-amid-widening-tech-war/).

3. Abnett, K. and Chestney, N., ‘With solar industry in crisis, Europe in a bind over Chinese imports’, Reuters, 4 February 2024 (reuters.com/ business/energy/with-solar-industry-crisis-europe-bind-over-chinese- imports-2024-02-06/).

4. Giovanni S., et. al., ‘Cleantech manufacturing: where does Europe really stand?’, Bruegel, 17 May 2023 (bruegel.org/analysis/cleantech- manufacturing-where-does-europe-really-stand-0).

5. EHPA, ‘EU plan will boost heat pumps but aims too low’, 16 March 2023 (ehpa.org/news-and-resources/news/eu-plan-will-boost-heat-pumps- but-aims-too-low/).

6. T&E, ‘A European Response to US IRA’, January 2023, (transportenvironment.org/discover/a-european-response-to-us- inflation-reduction-act/).

7. IEA, ‘Critical Minerals Market Review 2023’, July 2023 (iea.org/reports/ critical-minerals-market-review-2023).

8. BNEF, ‘The race to localize clean technology supply chains’, 7 September 2023 (about.bnef.com/blog/the-race-to-localize-clean-technology- supply-chains/).

9. Wood Mackenzie, ‘China to hold over 80% of global solar manufacturing capacity from 2023-26’, 7 November 2023 (woodmac.com/press- releases/china-dominance-on-global-solar-supply-chain/).

10. EBA, ‘Discussion Paper for the 7th High-Level Meeting of the European Battery Alliance’, 1 March 2023, (eba250.com/wp-content/uploads/2023/03/EBA_DiscussionPaper_Battery- Ministerial_01_03_2023.pdf).

11. Bloomberg, ‘Top wind firm’s profits fall even as clean energy booms in China’, 26 October 2023 (bnnbloomberg.ca/top-wind-firm-s-profits- fall-even-as-clean-energy-booms-in-china-1.1989819).

12. Blenkinsop, P., ‘EU sets critical mineral goals, but faces struggle to hit them’, Reuters, 18 December 2023 (reuters.com/markets/commodities/ eu-sets-critical-mineral-goals-faces-struggle-hit-them-2023-12-18/).

13. Joris, T. and Bertolini, M., ‘Reaching breaking point: The semiconductor and critical raw material ecosystem at a time of great power rivalry’, HCSS, October 2022 (hcss.nl/report/reaching-breaking-point- semiconductors-critical-raw-materials-great-power-rivalry/).

14. Rystad Energy, ‘Europe hoarding Chinese solar panels as imports outpace installations’, 20 July 2023 (rystadenergy.com/news/europe-chinese- solar-panels-imports-installations-storage).

15. Terazawa, T., ‘How Japan solved its rare earth minerals dependency issue’, WEF, 13 October 2023 (weforum.org/agenda/2023/10/japan-rare- earth-minerals/).

16. Mooney, A. et.al., ‘National Grid drops Beijing-backed supplier over UK power network fears’, Financial Times, 17 December 2023 (www.ft.com/ content/0a9887be-87df-4dcc-bdf5-38ee31cfe6b8).

17. IEA, ‘International Resource Strategy–National stockpiling system’, 26 October 2023 (iea.org/policies/16639-international-resource-strategy- national-stockpiling-system).