Wars kill and displace people, disrupt and reshape trade routes, remould security perceptions and, depending on the magnitude of fighting, reconfigure regional and potentially global orders. As Russia’s full-scale invasion of Ukraine (1) enters its eighth month, this Brief reviews the currently available data to produce a preliminary assessment of how the war has affected the EU’s eastern neighbourhood (2) on three levels: demographic, geoeconomic and geopolitical. While focusing on the immediate consequences of the conflict, the Brief also explores how trends set in motion or accelerated by the war may play out in the future. It concludes with reflections on what the war and related regional dynamics mean for the EU’s policy in the eastern neighbourhood.

Demographics

The war triggered the biggest displacement of people in the eastern neighbourhood since the Second World War. It has displaced and uprooted people from both the victim state and the aggressor state.

Data: European Commission, GISCO, 2022; Natural Earth, 2022; Ukrainska Pravda, ‘A record number of ships went through Ukrainian Danube ports over the past days’, 2022

Ukraine

According to the United Nations High Commissioner for Refugees (UNHCR), 7.2 million Ukrainians have left the country (3), which is 16 % of the population. While most of these people may eventually return home, some may never do. A recent survey among Ukrainian refugees in Poland revealed that 17 % do not have plans to return, while an overwhelming majority declared that sooner or later they intend to move back (4). Despite the fact that the war has been ongoing, from mid-April onwards Ukraine’s border service registered an inflow of returnees as the north of the country was progressively liberated. Since then, the numbers have grown; beginning in mid-May, Frontex recorded more Ukrainian citizens returning to the country than leaving it (5). However, the flow of returnees may abate in autumn until next spring as many refugees may prefer to spend the winter months in their host countries before returning to Ukraine.

In addition to refugees, a growing number of Ukrainians from Russian-occupied territories have been sent to ‘filtration camps’ and forcibly deported to Russia. It is estimated that up to 1.6 million Ukrainians (3.6 % of the population) have been sent to Russia against their will (6). The demographic impact of forced deportations is therefore substantial. It is unlikely that the bulk of the deportees will be able to return soon, in particular children orphaned by the war.

The adverse demographic impact is aggravated by military and civilian casualties. The UNHCR has recorded 5 916 civilian fatalities since 24 February (7). However, this is only the tip of the iceberg; civil activists have reported that morgues in Mariupol have registered 87 000 deaths since the beginning of the siege of the city (8). Estimated casualties among Ukrainian armed forces after six months of war are also high, at around 9 000 fatalities (9). This number is set to increase as the Ukrainian army transitions to more offensive operations. The announced mobilisation of reservists in Russia to make up for troop losses will prolong the conflict and thus the number of both civilian and military casualties will keep growing.

Deportations, refugees and casualties combined will exacerbate Ukraine’s demographic problems, as the country’s population has been on the decline for the last three decades already. A sharp demographic downturn might seriously hamper the reconstruction efforts and economic recovery of a post-war Ukraine.

Eastern neighbours

The war has affected the demographics of Ukraine’s neighbours too. Moldova has experienced the biggest inflow of refugees among the countries in the region.

In six months more than half a million Ukrainians crossed Moldova’s border and approximately 90 000 decided to stay in the country (10). As a result, refugees now account for 3 % of the Moldovan population. This represents an unprecedented, even if temporary, increase in population in the history of independent Moldova. Although it has put pressure on the country’s finances and healthcare system, citizens have welcomed the refugees. Attempts by political clients of the Kremlin to turn the local population against them have failed. While the number of Ukrainian refugees declined slightly during the summer, it is unlikely that many will return home soon because they originate predominantly from Odesa, Mykolaiv and Kherson Oblast, where Russia continues its ground operations and missile attacks.

Some Ukrainians from occupied territories in the south who escaped detention in filtration camps managed to drive across Russia’s North Caucasus and find shelter in the South Caucasus. Georgia shoulders the biggest burden as over 26 000 Ukrainians have found refuge in the country; fewer have settled in Armenia (489) and Azerbaijan (4 639) (11). Although the number of refugees from Ukraine is comparatively not as large as in Moldova, the South Caucasus has also been exposed to the demographic impact of the war.

Russia

The war has triggered a new wave of migration from Russia; twice as many Russians (419 000 citizens) left the country in the first half of 2022 than during the same period last year (12). The military mobilisation announced in September is set to drive the number of people fleeing the country even higher. In previous waves of migration, Russians headed mainly to western Europe, but this time communities have also emerged in the eastern neighbourhood.

Georgia has reported that in the first half of 2022 the number of Russians who entered the country increased by 355 % compared to the previous year (13). The increase is all the more spectacular given that Covid-19 led to a significant drop in the number of Russian tourists in 2021. However, this time around it is clear that not all Russian visitors are tourists; since January Russians have bought around 4 000 apartments in Georgia and more than 16 000 have obtained a residential permit (14). Armenia too has seen an unprecedented inflow of Russian migrants. The Armenian government reported that in the first half of 2022 around 40 000 Russian citizens settled in the country (15), a number which represents 1.4 % of Armenia’s population. These figures are likely to swell as Russians flee the draft. Since the announcement of mobilisation in Russia, Georgia has registered a 45 % increase in the number of Russians entering the country daily. (16)

Immigration has upsides and downsides. Immigrants reinvigorate economic activity; so far this year Russian citizens have set up more than 600 enterprises in Georgia, seven times more than in 2021 (17). Russians also bring hard currency; money transferred from Russia to Armenia in May amounted to USD 266 million, surpassing the previous monthly record from July 2013 (18). Russian immigrants also fuel consumption. However, there are potential negative effects too. Some of these newly-established companies may not be engaged in legal business activities, and both Georgia and Armenia will have to be vigilant that they are not involved in helping Russia circumvent sanctions. Immigration may have sociopolitical repercussions too. In Georgia, Russian immigration risks deepening polarisation as the country’s political forces have diverging opinions on the issue. The opposition advocates a stricter immigration policy for Russian nationals. Russia currently occupies 20 % of Georgia’s territory. The issue is highly emotional for Georgian people as memories of the 2008 military aggression are still fresh in their minds. Tensions and incidents between locals and Russian immigrants cannot be ruled out in the future, endangering social stability in the country.

Geoeconomics

The war has precipitated the disintegration of historic economic ties and has redrawn the geoeconomic map of the eastern neighbourhood.

Trade

Full-scale invasion has brought Ukraine’s trade with Russia, its main commercial partner before 2014, almost to a standstill. There are still pockets of economic interaction but even these are not sustainable in the long run. For example, Russia continues to pay Ukraine for the transit of gas and oil to Europe. But as the EU diversifies away from Russia’s energy imports these bilateral ties might wane, leading to a total economic decoupling between Russia and Ukraine.

The war has also impacted trade exchanges between Ukraine and Belarus. Before the war, Ukraine was Belarus’s second-biggest individual trade partner. This situation was highly advantageous for Minsk as out of USD 7 billion in bilateral turnover in 2021, USD 5.4 billion came from Belarusian exports (19). By siding with Russia, Belarus has largely lost the Ukrainian market. Minsk’s dependence on the Russian market is set to deepen, which in turn will facilitate the Kremlin’s de facto economic absorption of Belarus.

Conversely, the war has strengthened Ukraine’s commercial ties with Moldova. The volume of Moldovan exports to Ukraine increased massively in the first half of 2022, making Ukraine the second-largest individual export destination for Moldova The spike is explained by the re-export of oil products from Moldova. As Russia destroyed Ukraine’s major oil refineries, the country increased imports of fuel from or via neighbours. At the same time, the war disrupted Moldova’s exports to Russia (- 9 %) as Ukraine served as a transit route prior to the war. Exports to Russia are set to decline further as the Kremlin has imposed an embargo on Moldovan fruit and vegetable imports, which might cause Moldova to diversify more quickly away from the Russian market.

In the South Caucasus, only Armenia has managed to boost exports to Russia, likely mainly due to re-exports. Data shows that among the fastest growing exports to Russia were various types of vehicles, which became the second-biggest export item to Russia (20). Given that vehicle production has collapsed in Russia, the increasing volume of imports from Armenia is not that surprising. Even before the war Russia was Armenia’s main trading partner (21). If the current export dynamics persist, Armenia’s economic dependence on Moscow will deepen.

While Georgia’s and Azerbaijan’s exports to Russia slightly decreased, their imports grew significantly by 51 % and 32 % respectively (22). For Georgia, imports of petroleum products (which grew 280 %) and coal drove the increase. The increase in Azerbaijan’s imports from Russia is explained by higher grain imports. As prices for wheat rose globally, Baku appears to have moved to build a bigger national reserve stock. However in parallel it has also increased its imports of grain from Kazakhstan, indicating that Baku is trying to dilute its dependence on agricultural imports from Russia. If Azerbaijan’s imports of grain from Russia decline in the future, imports of gas may expand. As Europe moves away from Russian gas, Baku might increasingly rely on Russian gas to cover its domestic needs and instead send more gas from the Caspian Sea towards Europe.

Connectivity

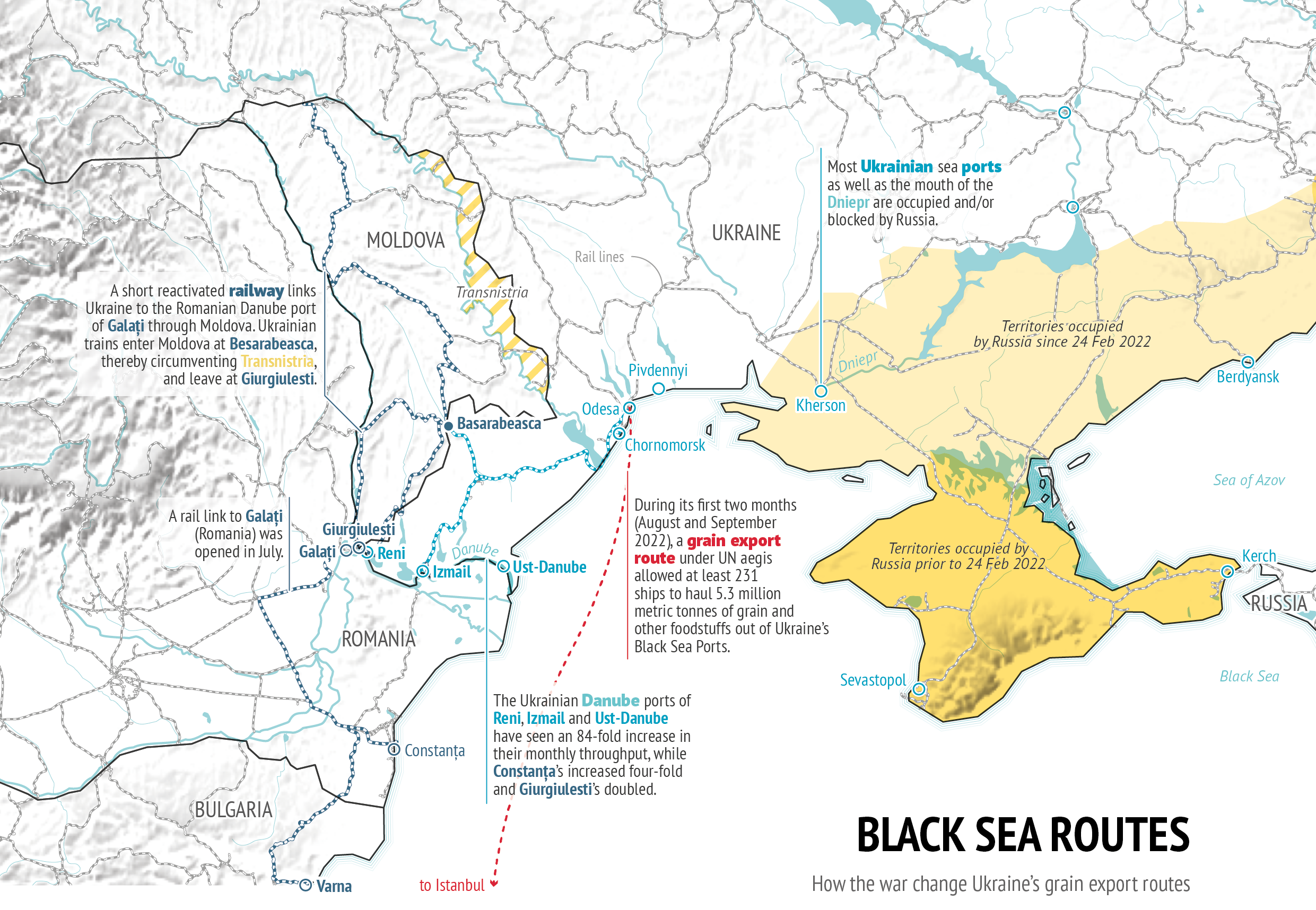

Connectivity in the region has seen significant disruption but also the emergence of new infrastructure linkages or more intensive use of those unaffected by the war and sanctions.

The destruction of refineries and suspension of trade with Belarus has forced Ukraine to redraw its import and export routes. With the blockade of the Black Sea (except for the grain exports deal under the aegis of the UN), through whose ports it shipped 90 % of its agricultural exports, Ukraine had to rely on ports on the Danube but also Romania’s and Bulgaria’s Black Sea ports. To reach the ports Ukraine and its neighbours had to repair or rebuild railway infrastructure and ensure faster transit for Ukrainian trucks. For example, the reconstructed Berezino– Basarabeasca section between Ukraine and Moldova allowed train traffic along this route to resume after 25 years of inactivity. The restoration of a rail link in Romania has allowed Ukrainian trains transiting Moldova to reach the Danube port of Galati directly for the first time in 22 years. To facilitate trade, Ukraine and Moldova have fully liberalised the transport of goods between their two countries.

All this has paid off in the short term. Still, the alternatives that emerged are not even close to matching the export capacities of Ukraine’s Black Sea ports. More investments and effort will be required to expand the existing routes and open new ones in order to make Ukraine less vulnerable to Russia’s maritime blockades.

Another of the war’s notable impacts on connectivity in the region is the higher volumes of goods shipped between Asia and Europe via the middle corridor through the Caspian Sea, which could increase up to six times this year (23). Freight between Azerbaijan and Kazakhstan increased 3.5 times in the first half of 2022 (24). Georgian railways reported the highest levels of freight traffic in 7 years (25). These upward trends are driven on the one hand by the suspension of the northern corridor through Russia and Belarus, and on the other hand by the opening of transit routes through the South Caucasus by European flagship transport companies. Still, while the traffic is certainly set to increase, the middle corridor may very soon reach its transit capacity. If states in the region are to take full advantage of the suspension of the northern route, more investments will be required to expand existing infrastructure but also to smoothen the transit of goods between different state jurisdictions.

Remittances

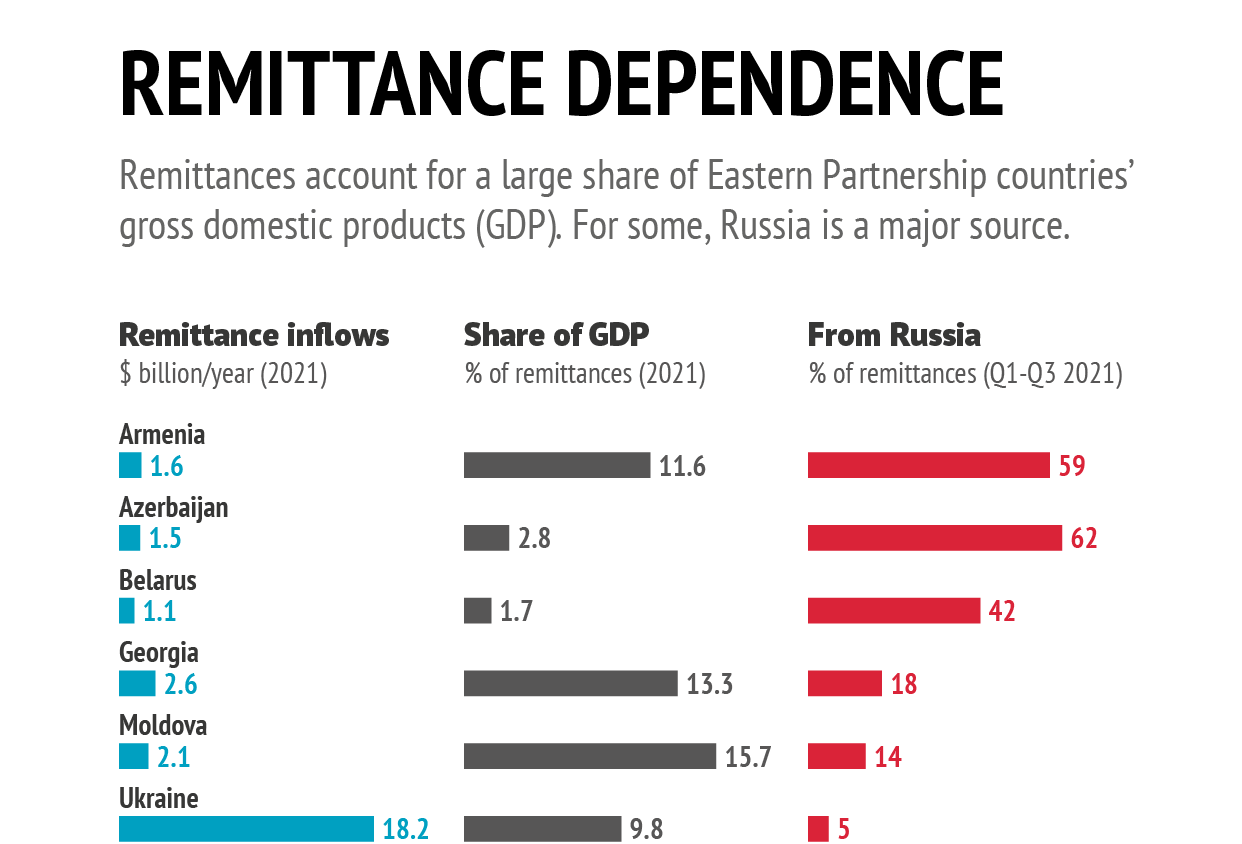

The war has had an impact on remittances from Russia in the region; however it is not easy to gauge it precisely as reports released by central banks often do not make a distinction between money transfers from Russian citizens and remittances sent by co-nationals working in Russia. In the case of Ukraine, the situation is clear. As a result of massive disruption of bilateral economic relations, direct money transfers between Russia and Ukraine have been curtailed. The situation is more ambiguous in the rest of the eastern neighbourhood. Azerbaijan, Georgia and Moldova reported a drop in money transfers from Russia in the first quarter of this year and a rebound in the second quarter (26). The statistics from Armenia are more nuanced and may help to cast light on the dynamics at play in the three above-mentioned states. The Armenian central bank reported a fall in remittances from Russia during the first half of 2022 and a significant increase in money transfers from Russian citizens from spring onwards (27). The decline in remittances points to the deteriorating economic situation in Russia while the greater inflow of money from Russian citizens might be related to the transfer of savings to a safer jurisdiction, migration, and relocation of business activities.

Data: World Bank, ‘Russia-Ukraine Conflict: Implications for Remittance flows to Ukraine and Central Asia’, 2022; World Bank, 'A War in a Pandemic', 2022

Looking ahead, Russia’s economic troubles are poised to sap its economic attractiveness and influence in the region. If Russia does not manage to reverse the current domestic economic trends, job opportunities and salaries for migrants are bound to shrink. This in turn may accelerate the exodus of migrant workers coming from the eastern neighbourhood towards alternative labour markets.

Geopolitics

The war has increased the security deficit in the eastern neighbourhood. It has compelled governments in the region to review defence policies and budgets, rethink foreign policy approaches and redouble efforts to join regional organisations. The war has also affected areas of protracted conflicts.

Hard power

The war has brought Belarus much closer to Russia not only economically but also militarily, to the extent that it has come to be perceived as a military ‘appendix’ of Russia. Belarus provides air space, logistics, munitions and repair facilities to the Russian armed forces. It also conducts military manoeuvres to keep some Ukrainian units away from combat in the east and south. The Kremlin will seek to increase and solidify its military presence in Belarus to threaten EU Member States and Ukraine. For Minsk, volunteers from Belarus fighting on Ukraine’s side are perceived as a potential security threat. Thus, the Russian military presence provides the regime with extra security, guaranteeing its survival in case of any internal destabilisation or insurgency.

The shock of war has compelled states in the eastern neighbourhood to double down on economic diplomacy.

The war has inadvertently turned Ukraine into the most powerful military actor in the eastern neighbourhood. Monthly spending on defence went up from USD 250 million in February to USD 3.3 billion in May 2022 (28). As the war intensified and Ukraine suffered losses in equipment and manpower, it has increasingly relied on Western munitions, equipment and training. Therefore, the war has accelerated Ukraine’s transition to Western defence equipment and standards. Given the fact that the Russian threat will not go away in the foreseeable future, Ukraine will have to maintain a sizeable army. Ravaged by war, Ukraine will face the financial challenge of sustaining this defence effort.

The war has led to an overhaul of Moldova’s national defence sector. Chronically underfunded prior to the war, Moldova’s defence budget has already been increased twice in 2022 by a total of 18.3 % (29). Chisinau also applied for greater financial assistance from the EU’s European Peace Facility (EPF); the total granted assistance practically doubled Moldova’s defence budget. Domestic and European resources combined are paving the way for the gradual modernisation of the national armed forces’ defence capabilities.

In the case of the South Caucasus, Russia’s aggression against Ukraine has only reconfirmed that there is a need to invest more in defence. Even before the war, in 2021, Georgia and Armenia increased their military spending and Azerbaijan did likewise despite its victory in the 2020 war with Armenia. Azerbaijan plans to increase its military budget from USD 2.6 billion to USD 2.8 billion by 2025 (30) to maintain its dominance over Armenia. In order to avoid the military gap becoming even bigger between the two, Armenia is likely to try to keep up the pace of expenditure. As Russia experiences a shortage of munitions and weapons, Baku and Yerevan, who possess large stocks of Russian-made weapons, will increasingly look to other military suppliers in the East and West. The 2021 hike in the defence budget in Georgia was modest. Given the more unstable environment in the region, a greater increase in defence spending might not be ruled out.

Foreign Policy

Defence spending is not the only way to ensure security; economic diplomacy and membership in organisations and alliances can play an important role in ensuring national security too.

Three states in the eastern neighbourhood – Georgia, Moldova and Ukraine – decided to apply for EU membership sooner than they had initially planned. EU membership is not only considered as a means of bolstering the economy but also of adding an extra layer of security against a myriad of threats coming from Russia. While quick membership is not on the cards, candidate status greatly facilitates sectoral integration into the EU. In addition Ukraine decided to apply for NATO membership. On the other side of the political spectrum, Belarus applied for membership of the Shanghai Cooperation Organization, perhaps in an attempt to secure an additional track of engagement with China and thus dilute its overwhelming economic dependence on Russia.

The shock of war has compelled states in the eastern neighbourhood to double down on economic diplomacy, opening up the region even more to third-party actors. Embargos and the risk of Russia cutting off gas supplies have forced Moldova to send out trade missions to access new export markets and secure alternative gas imports.

Armenia has sought to double gas imports from Iran as part of a decade-old gas-for-electricity swap deal, while also reaching out to the United States for cooperation in the civilian nuclear field. Azerbaijan has pledged to double gas exports to Europe by 2027. Ukraine has sought to muster financial, military and diplomatic support behind its defence against Russia’s aggression. Even if only half of the projects and missions are successful, Russia’s economic power to coerce countries in the region will be further diminished.

Protracted conflicts

As Russia is involved in all protracted conflicts in the eastern neighbourhood, the war against Ukraine has inevitably affected the situation in these places. The Kremlin has turned to separatist regions to compensate for the deficit of manpower in Ukraine. Russia has redeployed some of its troops from Nagorno-Karabakh, South Ossetia and Abkhazia to Ukraine. Russia has also pushed its proxies in Tskhinvali and Sukhumi to send local paramilitary units into war with Ukraine. In Transnistria, Moscow has conducted recruitment campaigns for the same purpose. The shrinking of Russia’s military footprint in South Ossetia and Abkhazia has not changed the fundamentals; Tbilisi does not have enough military power or political will to try to restore territorial integrity by force.

In contrast, the weakening of Russia has correlated with a resurgence of violence between Armenia and Azerbaijan. As Russia was reeling from defeat in Kharkiv, the two sides engaged in September in the most violent escalation since the 2020 ceasefire. It is important to note that the combat was mainly concentrated along the state border between Armenia and Azerbaijan and less so in contested Nagorno-Karabakh. As a result of infighting, Armenia experienced additional territorial losses. It appears that Baku perceives Russia’s temporary weakness as a window of opportunity to reclaim the entire Nagorno-Karabakh region more quickly and thus render Russia’s peacekeeping presence there (whose mandate expires in 2025) unwarranted. If this is an accurate reading of Baku’s intentions, then the message behind the flare-up of violence is for Armenia to recognise Azerbaijan’s sovereignty over the disputed region or risk losing more of its own sovereign territory.

Russia’s weakness has not only upset the military balance in the region, but also reshaped the format of talks between Baku and Yerevan. In the wake of the 2020 war, one-to-one talks mediated by Moscow emerged as a new format. The war in Ukraine has diminished Russia’s role as a mediator and elevated that of the EU and the US. Since Russia’s full-scale invasion, Armenian and Azerbaijani officials have travelled for talks more often to Brussels than to Moscow or Sochi. Importantly, after failed appeals to Russia, Yerevan turned to the US to broker the ceasefire with Azerbaijan in September. The deterioration of Russia’s military capabilities and failure to protect its ally have tarnished its reputation and are set to undermine its mediating role on this issue.

The status quo is evolving in the Transnistrian conflict too. The war has made it impossible to hold meetings within the 5+2 negotiations format, which includes Russia and Ukraine. The discussions have moved increasingly to a one-to-one format where both sides address everyday economic and social issues. The war has also disrupted trade between Transnistria and its second-biggest export market – Ukraine – as the government in Kyiv sealed off the segment of border with the separatist region. As a result of the war the breakaway republic has had to rely exclusively on exports and imports via territory controlled by the Moldovan authorities. Thus, the war has shifted the economic balance moderately in favour of Chisinau, creating conditions for further economic reintegration of Transnistria into Moldova.

The most important change the war has brought, however, is in how the conflict is perceived. It had previously been regarded as the most solvable conflict in the region. After 30 years of unbroken ceasefire, military escalation was not considered as a realistic scenario. At the same time, international partners hoped that confidence-building measures in time would pave the way for political talks between the sides. The full-scale invasion of Ukraine has changed this perspective; reviving the risks of remilitarisation of the conflict. As a result, the entire philosophy around conflict management has changed away from fostering confidence in finding resolution in the future to more conservative objectives, such as preventing destabilisation and ensuring smooth communication between sides to avoid escalatory dynamics. As long as the war drags on in Ukraine, the return to the logic of settling the Transnistrian conflict is not feasible. That being said, Russia’s economic weaknesses and Transnistria’s increasing dependence on the EU market create favourable premises for settling the conflict in the long run. This potentially positive trajectory will depend on the outcome of the Russian-Ukrainian war.

Policy considerations for the EU

Wars are big catalysts for change; the EU’s policy in the eastern neighbourhood is not an exception. In response to the invasion, the EU extended the enlargement process to the East and began channelling funds to supply Ukraine with heavy weapons. These decisions are revolutionary and deserve praise; but it is too early for complacency. The EU has to seize the initiative and maintain this newfound momentum of engagement in its neighbourhood. In order to succeed it will require speed, sustainability and resources. The EU will have to be able to act fast, pre-empt negative developments and foster benign changes in the region, and allocate more human and financial resources towards both ends. All this will serve the EU’s security interests and accelerate its transformation into a more coherent and credible foreign policy actor.

The EU will need to sustain financial support to states in the region which continue to accommodate Ukrainian refugees. The EU may also need to speed up the relocation of refugees to Europe in order to lift the burden from more fragile accommodating states in the East.

Still, the lion’s share of the financial support will need to go to Ukraine, helping the government in Kyiv to accommodate and reintegrate refugees and internally displaced people. As winter is coming, the urgency of the task cannot be ignored. The EU has taken important steps to remove import tariffs on Ukrainian goods, increased tariff-free quotas for Moldova, and liberalised road transport within the two countries. As these agreements are set to expire in one year while the impact of the war is set to last, the EU has to extend these benefits over a longer period. For Moldova, the decision to lift all import tariffs will be of significant help for a country against which Russia is sharply escalating economic warfare. In the South Caucasus, the EU has to monitor the situation closely and curb any attempts at the evasion of sanctions, but at the same time look for ways to boost Georgia’s and Armenia’s exports to the EU.

A Ukraine which is capable of defending its borders is in the EU’s best interest.

It is high time to invest more in greater connectivity with the eastern neighbours. The synchronisation of Ukraine’s and Moldova’s power systems with the Continental European electricity grid has already paid off as Europe has begun importing electricity from Ukraine. Similarly, the EU has to provide more support to Ukraine and Moldova to expand road and railway infrastructure connecting them with EU Member States. Also, more investments in the southern corridor promise to be economically beneficial for states in the region and in the EU. In the South Caucasus, the EU could use its growing mediating role to contribute in the mid-term to the reopening of the borders between Armenia and Azerbaijan and to the modernisation of infrastructure connecting both. The EU could help Georgia to connect to Europe’s electricity grid via the Black Sea bed into Romania.

The war has set in motion profound geopolitical transformations. The enlargement policy now applies to three states in the eastern neighbourhood. The next step would be to allocate financial and human resources for pre-accession funds and monitoring of reforms respectively. As the three states pursue different trajectories, the Eastern Partnership (EaP) programme must meet the challenge of how to combine inclusivity amidst greater differentiation among participant states. One possible way to go ahead is to preserve and to amplify the multilateral dimension, especially the non-governmental one, while customising bilateral engagements even more. Still, it must be borne in mind that any attempt to adapt the EaP will fail without ownership of the local stakeholders.

One area where the success or failure of the Neighbourhood Policy will be decided is security. Because of the war and its consequences, states in the region face a security deficit. The EU is already an important developmental player in the region, now it has to assume a greater security role too. For example, it can regularly allocate funds from the EPF for Georgia, Moldova and Ukraine in order to sustain ongoing military modernisation now and in the long term. In Ukraine, the European Union Advisory Mission (EUAM Ukraine) has been adapted to new needs on the ground. It is time to back it with a robust CSDP mission, which will ensure the training of Ukrainian military personnel. A Ukraine which is capable of defending its borders is in the EU’s best interest. In Moldova too, the European Union Border Assistance Mission to Moldova and Ukraine (EUBAM) and Frontex have performed important tasks during the refugee crisis. The launch of the EU support hub for internal security and border management in Moldova is a step in the right direction, but the scope of the initiative has to be expanded and probably transformed into a proper CSDP mission encompassing training assistance for the intelligence and defence sector.

The EU has to keep raising its profile and cement its role as mediator between Armenia and Azerbaijan with the aim of ensuring a gradual normalisation of relations between Baku and Yerevan. To avert further outbreaks of violence and keep up the momentum behind negotiations, close diplomatic coordination between the EU and the US will be required. There is an opportunity for the EU to enhance its position and role in the Transnistrian conflict too. While a solution to the conflict is not on the cards in the short run, the EU could become a good-faith facilitator of one-to-one talks between Chisinau and Tiraspol, to ensure stability but also to speed up Transnistria’s integration into Moldova’s economic and legal space.

Finally, as the EU moves to strengthen its security, economic and diplomatic position in the region, it is essential to work closely with states and institutions whose agenda is in line with the EU’s objectives. It will be important to build up on cooperation developed in particular over the last seven months with the United States, NATO and international financial institutions, in order to amplify the effect of the EU’s efforts to stabilise the eastern neighbourhood, ensure security and support economic development.

References

The author is grateful to Stefan Meister, Florence Gaub and Sabine Fischer for insightful comments on early drafts of this Policy Brief. The author would also like to thank Tijs Cornelis van de Vijver for his research assistance.

1. Hereafter referred to as ‘the war’.

2. The EU’s eastern neighbourhood encompasses six states: Armenia, Azerbaijan, Belarus, Georgia, Moldova and Ukraine.

3. UNHCR, ‘Refugees from Ukraine recorded across Europe’, 13 September 2022 (https://data.unhcr.org/en/situations/ukraine).

4. Schengen Visa Info, ‘Over 20 % of Ukrainian refugees in Poland intend to return to their homeland before Winter’, 12 September 2022 (https:// www.schengenvisainfo.com/news/over-20-of-ukrainian-refugees-in- poland-intend-to-return-to-their-homeland-before-winter-survey- reveals/).

5. NAPA, ‘Frontex: More Ukrainians are returning than leaving the country’, InfoMigrants, 6 June 2022 (https://www.infomigrants.net/en/ post/40990/frontemore-ukrainians-are-returning-than-leaving-the- country).

6. Blinken, A. J., ‘Russia’s “Filtration” operations, forced disappearances, and mass deportations of Ukrainian citizens’, United States Department of State, 13 July 2022 (https://www.state.gov/russias-filtration- operations-forced-disappearances-and-mass-deportations-of- ukrainian-citizens/).

7. UNHCR, ‘Ukraine: Civilian casualty update 19 September 2022’, 19 September 2022 (https://www.ohchr.org/en/news/2022/09/ukraine- civilian-casualty-update-19-september-2022).

8. EuromaidanPress, ‘87,000 killed civilians documented in occupied Mariupol’, 30 August 2022 (https://euromaidanpress.com/2022/08/30/87000-killed-civilians-documented-in-occupied- mariupol-volunteer/).

9. Zinets, N., ‘Almost 9,000 Ukrainian military killed in war with Russia’, Reuters, 22 August 2022 (https://www.reuters.com/world/europe/ almost-9000-ukrainian-military-killed-war-with-russia-armed- forces-chief-2022-08-22/).

10. ‘Refugees from Ukraine recorded across Europe’, op.cit.

11. Ibid.

12. Keffer, L., ‘Since the beginning of the year, 419 thousand people left Russia’, Kommersant, 6 September 2022 (https://www.kommersant.ru/ doc/5547632?from=top_main_9).

13. JamNews, ‘More than 135,000 Russian citizens entered Georgia in June’, 28 July 2022 (https://jam-news.net/more-than-135000-russian- citizens-entered-georgia-in-june/).

14. Dvali, G. and Vorontsov, I., ‘Around 23 thousand Russian citizens own real estate in Georgia’, Kommersant, 9 September 2022 (https://www. kommersant.ru/doc/5548522).

15. Harutyunyan, S., ‘In the first half of 2022, about 40 thousand Russians settled in Armenia’, RFL, 4 August 2022 (https://rus.azatutyun. am/a/31973100.html).

16. La Presna Latina, ‘“None of us want to go to war”: Russians flee to Georgia amid mobilization’, 27 September 2022 (https://www.laprensalatina.com/none-of-us-want-to-go-to-war-russians-flee-to- georgia-amid-mobilization/)

17. ‘TI – Georgia reveals Georgia’s increased economic dependency on Russia’, Civil.ge, 3 August 2022 (https://civil.ge/archives/502946).

18. Zagorovskaya, Y., ‘Armenia to support relocation’, Kommersant, 26 July 2022 (https://www.kommersant.ru/doc/5480675).

19. Ilex, ‘From miracle to shock – What’s next for Belarusian exports?’, 14 March 2022 (https://ilex.by/ot-chuda-do-shoka-chto-zhdet- belorusskij-eksport/).

20. Mejlumyan, A., ‘Armenian trade with Russia raises questions about re- exports’, Eurasianet, 31 August 2022 (https://eurasianet.org/armenian- trade-with-russia-raises-questions-about-re-exports).

21. Directorate-General for Trade, ‘EU trade in goods with Armenia’,2 August 2022 (https://webgate.ec.europa.eu/isdb_results/factsheets/ country/details_armenia_en.pdf).

22. Transparency International - Georgia, ‘Georgia’s economic dependence on Russia: Impact of the Russia-Ukraine war’, 3 August 2022 (https:// transparency.ge/en/post/georgias-economic-dependence-russia- impact-russia-ukraine-war); Interfax-Azerbaijan, ‘Russian Azerbaijani trade turnover increase by 21 % in seven months, export to Russia dropped 3 %’, 17 August 2022 (http://interfax.az/view/874331).

23. Gabritchidze, N., ‘Georgia, Azerbaijan see surge in transit demand amid Russia’s isolation’, Eurasianet, 2 June 2022 (https://eurasianet. org/georgia-azerbaijan-see-surge-in-transit-demand-amid-russias- isolation).

24. Aliyev, M., ‘Tokayev’s special mission’, ASTNA, 24 August 2022 (https://astna.biz/ext/news/2022/8/free/region-caspian/ru/2644.htm).

25. Agenda.ge, ‘2022 freight income highest in 7 years – Georgian Railway’, 8 August 2022 (https://agenda.ge/en/news/2022/3001).

26. National Bank of Georgia, ‘Money transfers’ (https://nbg.gov.ge/en/ page/money-transfers); Uvarchev, L., ‘Money transfers from Russia to Azerbaijan increased by 4.9 times’, Kommersant, 15 September 2022 (https://www.Kommersant.ru/doc/5560761).

27. PanArmenian.Net, ‘Transfers from Armenians in Russia declined, from Russians to Armenia increased’, 16 May 2022 (https://www.panarmenian.net/rus/news/300300/).

28. ‘Ukraine shifts gear with debt deals as war takes toll on finances’, The Financial Times, 25 July 2022 (https://www.ft.com/content/65b63b3a- bb58-4b5a-b827-15ce48b24c1d).

29. Mirca, C., ‘Budget for Ministry of Defence will be increased by14.5 million’, TVM, 25 August 2022 (https://tvrmoldova.md/ article/8d03385a35a5c9cb/bugetul-pentru-ministerul-apararii-va-fi- majorat-cu-14-5-milioane-lei.html).

30. Natiqqizi, U., ‘After war victory, Azerbaijan keeps increasing military spending’, Eurasianet, 12 May 2022 (https://eurasianet.org/after-war- victory-azerbaijan-keeps-increasing-military-spending).